The neighbors’ porch lights are going dark one by one.

Across the fence, the evening noises have settled into the background. You and your spouse are still outside, lingering a little longer before calling it a night.

The coffee on the patio table has long since lost its warmth.

The conversation moves the way it usually does.

The kids. Work. Weekend plans. A vacation you may or may not take next year.

Then, almost without warning, one of you asks a question that shifts the conversation.

“Have we actually built enough?”

Enough for the years when the paychecks no longer arrive twice a month and the routines that have shaped your lives begin to change.

The question hangs there for a moment.

It is one of the most important financial conversations a couple can have, yet it often gets pushed further down the road. Careers demand attention. Family schedules stay full. Retirement remains a distant landmark somewhere beyond the horizon.

The Difference Between Having Savings and Having Options

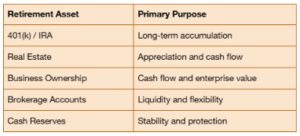

Most couples spend decades doing the responsible things. They build careers, pay down debt, raise families, contribute to retirement accounts, and steadily create a life that feels secure.

But one of the questions I encourage families to ask is whether they are building assets that simply accumulate value or assets that can actively create flexibility later in life.

A rental property may appreciate and generate income, but it also comes with its own operational realities.

A business can generate cash flow and potentially create enterprise value, but it requires leadership and execution.

Each asset serves a different purpose.

That is why the strongest long-term plans are rarely built around a single pillar.

They are built around multiple sources of stability working together.

The goal is not to choose one category and ignore the others.

The goal is understanding how each piece contributes to the bigger picture.

One Lesson I Learned the Hard Way

Before becoming a franchise consultant, I owned a healthy vending machine business.

On paper, it looked like a franchise.

It wasn’t.

The business grew significantly. But I also learned something important.

The business depended heavily on me. If I stopped moving, parts of the business slowed down with me.

If I wasn’t identifying new locations, managing relationships, or solving operational challenges, growth stalled.

That experience completely changed how I evaluate business opportunities today.

When I sit down with couples, I often encourage them to look beyond potential income and talk through questions together.

What systems already exist?

What support is available?

Can the business eventually become more operationally efficient without requiring every hour of your week?

Why More Couples Are Looking Beyond Traditional Retirement Planning

Many of the couples I speak with are not trying to leave their careers tomorrow.

In fact, most genuinely enjoy what they do.

The conversation is usually less about escaping work and more about expanding future options.

Because when you reach your forties, fifties, or early sixties, the financial discussion often becomes less about accumulation and more about flexibility.

You start asking different questions.

Questions such as:

“What if one spouse wants to keep working while the other is ready for something different?”

“What if we want more time with family?”

“What if healthcare costs increase?”

“What if we simply want more control over how we spend our time?”

They are lifestyle questions that often require financial structures that create choices.

The Mistake I Encourage Couples to Avoid

One of the biggest trapdoors I see is treating business ownership as a solution before fully understanding the problem it is supposed to solve.

Sometimes people are reacting to burnout.

Sometimes they are reacting to uncertainty.

Sometimes they are reacting to a difficult year at work.

But major financial decisions made during emotionally charged seasons deserve more time, not less.

I also encourage couples to evaluate timing honestly.

If a major relocation, health issue, career transition, or family change is already underway, adding ownership to the mix may not be the right move yet.

And that is okay.

A good opportunity today should still be a good opportunity after thoughtful evaluation.

A Better Conversation to Have

Instead of asking, “How much money will we need?”

Try asking:

“What kind of life are we trying to create?”

Because once you answer that question, the financial decisions often become clearer.

You begin thinking less about retirement as a finish line and more as a stage of life that should offer freedom, flexibility, and choices.

Final Thoughts

If you and your spouse have started having conversations about what the next ten, fifteen, or twenty years might look like, you are already asking the right questions.

The objective is not to predict every twist and turn the future may bring.

The objective is to build enough flexibility that the two of you can shape the next chapter together, instead of having it shaped for you by circumstances.

Business ownership may or may not belong in that plan. But it is worth understanding before deciding.

If you and your spouse are starting to think more seriously about what comes after the paychecks stop, or whether your current structure supports the life you want long-term, that is exactly the kind of conversation we have at Aspen Business Consultants.

This is where structured guidance tends to matter most. I would be happy to have a thoughtful introductory conversation with you here.